Are you eligible for VA Benefits? Learn how to buy a home using your VA Benefits in this post. Both Paul and Dianna Howell with The Howell Group – KW work with many clients who have VA Benefits. By the end of this article, you will have a better understanding of how to become a homeowner using your VA Benefits!

Here’s a video you can watch that covers who is eligible for VA Benefits and the benefits of using VA Loans to buy a house:

Let’s talk about how to use your VA Benefits to buy a house in Alabama. There are millions of veterans and active service members that are eligible for VA Loans. First, we’ll cover who is eligible for a VA Loan. Then we’ll discuss the benefits of using a VA Loan and what VA Loans cannot do.

Who is Eligible for a VA Loan?

In order to use a VA Loan, you first need to know who is eligible for a VA Loan. Veterans, active duty service members, National Guard members and reservists must meet the basic requirements set forth by the Department of Veteran Affairs. You must have an honorable discharge in order to be eligible to apply for a VA Loan.

Here are the conditions:

You have served 90 consecutive days of active service during wartime

OR you have served 181 days of active service during peacetime

OR you have more than 6 years of service in the National Guard or Reserve

OR you are the spouse of a service member who has died in the line of duty or as a result of a service-related disability

You must have an Honorable Discharge from the military in order to be eligible to use your VA Benefits.

For more detailed information, please visit the VA Loans website: https://www.valoans.com/eligibility/

In order to apply for a VA Loan, you need the two following documents:

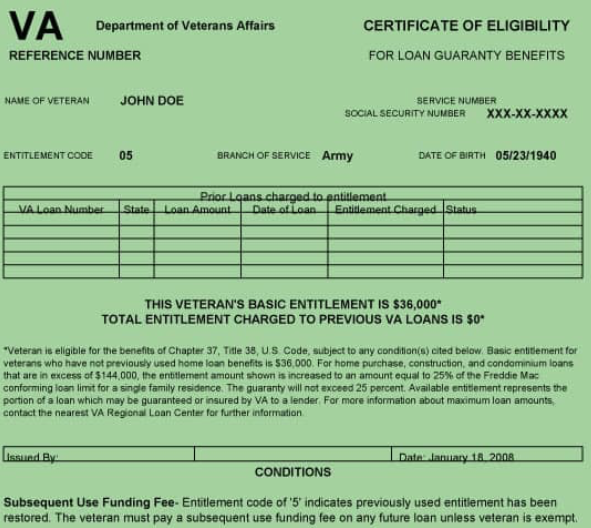

VA Certificate of Eligibility & Entitlement

Learn more about VA Eligibility and the VA Certificate of Eligibility here: https://www.valoans.com/eligibility/certificate-of-eligibility/

DD214

Please not that even those eligible to apply for VA Loans still need to be able to qualify for a VA Loan before using one. Be sure to choose a mortgage lender who is experienced with working with VA Loans. Better yet, find a lender that is a Certified Veteran Mortgage Specialist.

Work with your lender closely throughout the process of using your VA Loan so you know what your options are. We at The Howell Group work closely with our preferred lenders that specialize in VA Loans in the Greater Birmingham area. If you need help finding a VA Specialist lender, e would love to refer you to one. Please see our contact details at the end of this post.

What Are the Benefits of Using a VA Loan?

There are many benefits to using a VA Loan. However, every VA Loan is different due to the individual’s circumstances, so please make sure to work closely with your lender.

- In most cases eligible buyers are not required to have a down payment.

- No PMI or monthly private mortgage insurance.

- Sellers can pay all of buyer’s loan related closing costs and up to 4% in concessions.

- Lower interest rates. VA loans have the lowest interest rates of all loan types.

- No prepayment penalties. You can pay off the VA loan early.

- You can refinance your VA loan to a lower monthly payment with a new interest rate. You can also refinance a loan other than VA into a VA loan program.

- Second Tier Entitlement: veterans may be able to buy a second home with unused remaining or restored loan entitlements.

- Assumable Mortgage with VA and/or lender approval.

- Foreclosure Avoidance Advocacy. VA has staff who advocated on behalf of the homeowner to find alternatives to foreclosure.

What VA Loans Cannot Do

While VA Loans have many advantages, there are still some things that they cannot do. One main fact it that using a VA Loan does not guarantee that the home is free of defects. It is still up to the buyer to do their due diligence and inspections on the home.

Requirements for VA Loans:

1. Eligible Veteran who has available entitlement.

2. Loan must be for an eligible purpose.

3. Veteran must occupy or intend to occupy the property as a home within a reasonable period of time after closing the loan. There are some exceptions and you can speak with your lender.

4. Veteran must be a satisfactory credit risk. The income of veteran and/or spouse must be sufficient to meet the mortgage payments and cost of owning a home.

Learn more about using your VA Benefits to buy a home in Alabama on these sites: www.valoans.com and www.veteransunited.com

VA Loan Myths

Now that we’ve covered who is eligible for VA Loans and some of the benefits of using a VA Loan as well as what VA Loans cannot do, let’s talk about some of the VA Loan myths out there. VA Loans are often misunderstood by inexperienced lenders and realtors, which is why it’s so important to have specialists by your side during the buying or selling process.

Here are the five most common VA Loan myths:

1. The VA loan is a government backed loan

The first myth is that a VA Loan is backed by the government. This isn’t true and in addition, as mentioned earlier, one of the benefits of using a VA Loan is that there is no PMI.

2. VA home loan is only available for one time use

The second myth is that you can only use your VA Benefits to apply for one VA Loan. While every VA Loan is different, most people don’t realize that the VA loan can be used more than once.

3. VA home loan benefits have an expiration date

This third myth is very common. Contrary to popular belief, VA home loans do not have an expiration date. As long as you are eligible for VA Benefits and qualify for a VA Loan, you can use your loan your entire life.

4. A borrower can only have one VA loan at a time

This fourth myth is similar to myth #2 and it is important to note that not only can you use your VA Benefits more than once, but that if you qualify you can use more than one VA Loan at a time. Once again, every loan is unique, so work closely with your lender.

5. Loan amount

A lot of people think that there is a loan amount limit for VA Loans. The answer to this myth is both yes and no. Please watch this video where our Certified Veteran Mortgage Specialist, Chris Montz, answers this question:

VA Credit Myths

In addition to VA Loan Myths, there are also VA Credit Myths! Three of the most common credit myths concerning VA Loans are listed below. To hear more about them, please watch this video:

Here’s a quick summary on three common VA Credit Myths:

Depending on your situation, you may be able to qualify for a VA Loan two years after you filed for bankruptcy.

Ask your lender about your options if you have had a foreclosure. Sometimes you may be eligible for another VA Loan after two years.

If you have filed for a chapter 12 bankruptcy, talk to your lender about your options with your VA Loan. In some situations you may qualify for a VA Loan.

Like we’ve mentioned before, every VA Loan is different, so if you have questions about your VA Benefits, VA Loan, or even credit questions, please make sure you call a lender that specializes with VA Loans.

Have More Questions About VA Benefits or Are You Ready to Start Using Them?

If you have questions about the VA Loan process or are looking to buy a home in the Birmingham area, we would love to be of service! Please contact Dianna Howell with The Howell Group at 205-568-5435 or dianna.howell@kw.com

The Howell Group also works closely with mortgage lenders in the Greater Birmingham area that specialize in VA Loans. Please reach out if you need a reference for a lender!

You can search for homes in Alabama here: https://diannahowellrealtor.com/locations/shelby-county-al/pelham/

LINK INFORMATION:

Using your VA Benefits to buy a home in Alabama: www.valoans.com or www.veteransunited.com

VA Eligibility: https://www.valoans.com/eligibility/

VA Certificate of Eligibility & Entitlement: https://www.valoans.com/eligibility/certificate-of-eligibility/

VA website: https://www.va.gov

Search for homes in Alabama: https://www.thehowellgroupofalabama.com

Download our FREE Homebuyers Guide: https://mailchi.mp/d0dba8656669/homebuyersguide

Read our 6 Steps to Buying a Home in Alabama Blog: https://diannahowellrealtor.com/buying/6-steps-to-buying-a-home-in-alabama/

Read our Tips for First Time Homebuyers Blog: https://diannahowellrealtor.com/buying/tips-for-first-time-homebuyers/